The table of the Average Daily Range for 28 currency pairs from 2014 to 2025. (the numbers are rounded)

Average Daily Range of Gold (XAUUSD) was added to the table

Average Daily Range of Silver (XAGUSD) was added to the table.

For the Average Daily Range of Exotic Forex pairs see here

Help:

- Use the filter for CURRENCY PAIR tab (click on it) to sort it alphabetically

- Use the filter of each year to sort currency pairs based on the least and most volatility according to that year

- Use search to find a currency pair, or a specific category for example USD for USD/JPY, EUR/USD, AUD/USD, etc.

Forex Average Daily Range Table

| CURRENCY PAIRS | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AUD/CAD | 76 | 98 | 86.5 | 69.5 | 65 | 60 | 80 | 62.5 | 72 | 69 | 55.5 | 57 |

| AUD/CHF | 70.5 | 106.5 | 86 | 60.5 | 60.5 | 52.5 | 70 | 57.5 | 65 | 57 | 49.5 | 46 |

| AUD/JPY | 82.5 | 111 | 121 | 74 | 80 | 65 | 90 | 76 | 104 | 97 | 115.5 | 97 |

| AUD/NZD | 71 | 105 | 86 | 70 | 62 | 52 | 63 | 54.5 | 61 | 59 | 51.5 | 51 |

| AUD/USD | 73.5 | 92 | 84.5 | 59 | 62.5 | 48 | 81 | 66 | 81.5 | 73 | 55 | 57 |

| CAD/CHF | 63 | 100 | 77 | 61 | 59 | 48.5 | 58 | 54.5 | 60 | 52 | 45 | 44 |

| CAD/JPY | 76.5 | 100 | 118.5 | 77.5 | 76.5 | 61 | 76 | 72 | 102 | 99 | 115 | 96 |

| CHF/JPY | 79 | 146 | 115 | 81 | 75.5 | 58.5 | 82 | 71 | 116 | 128 | 139 | 125.5 |

| EUR/AUD | 128 | 187 | 165 | 112 | 107 | 101 | 166 | 117.5 | 139 | 131 | 104.5 | 120 |

| EUR/CAD | 105 | 164 | 151 | 114 | 108 | 79.5 | 117 | 96 | 107.5 | 98 | 76.5 | 88.5 |

| EUR/CHF | 23 | 96 | 53 | 52 | 59 | 47 | 46 | 44.5 | 63 | 55 | 55.5 | 48.5 |

| EUR/GBP | 44 | 70 | 87 | 67 | 54 | 62 | 77 | 54.5 | 64 | 51 | 37 | 41 |

| EUR/JPY | 97 | 137 | 126.5 | 88 | 103.5 | 73.5 | 96 | 79 | 128 | 131 | 158 | 128.5 |

| EUR/NZD | 131 | 211 | 179 | 135 | 121 | 112 | 169 | 129.5 | 152 | 144 | 116.5 | 129 |

| EUR/USD | 74 | 124 | 90 | 78 | 85 | 55 | 85 | 68 | 91.5 | 81 | 65 | 75 |

| GBP/AUD | 149 | 234 | 222 | 151 | 151 | 157.5 | 187 | 137.5 | 159.5 | 148 | 124 | 136 |

| GBP/CAD | 126 | 184 | 202 | 148 | 141 | 137.5 | 158 | 123 | 138.5 | 121 | 95.5 | 108 |

| GBP/CHF | 91 | 171 | 152 | 105 | 95 | 103 | 112 | 93.5 | 106 | 84 | 81 | 74 |

| GBP/JPY | 133 | 171 | 226.5 | 138.5 | 134 | 125 | 142 | 119 | 169 | 164 | 200 | 160 |

| GBP/NZD | 168 | 279 | 246 | 179 | 167 | 172.5 | 196 | 153 | 173.5 | 162 | 136 | 147 |

| GBP/USD | 87 | 123 | 149 | 103 | 110 | 100 | 131 | 101 | 127 | 109 | 81.5 | 90 |

| NZD/CAD | 79 | 105 | 95 | 78 | 68 | 60 | 76 | 65 | 72.5 | 68 | 55 | 56 |

| NZD/CHF | 66 | 106 | 82 | 61 | 56 | 49.5 | 64 | 55.5 | 60 | 52 | 45 | 42 |

| NZD/JPY | 80 | 110.5 | 110 | 69 | 72 | 61 | 82 | 73 | 93 | 88 | 99 | 84 |

| NZD/USD | 72 | 94 | 84 | 63 | 59 | 49 | 73 | 64 | 76.5 | 68 | 52 | 54 |

| USD/CAD | 67 | 116 | 121 | 89 | 88 | 65 | 99.5 | 86 | 100 | 86 | 63 | 71 |

| USD/CHF | 58 | 115 | 79 | 69 | 64 | 53 | 66 | 58 | 78 | 71 | 59.5 | 62 |

| USD/JPY | 73.5 | 92.5 | 120.5 | 90 | 70.5 | 58 | 74 | 62.5 | 117.5 | 123 | 157.5 | 133 |

| XAU/USD(gold) | 168 | 160 | 183 | 126 | 123 | 155 | 305 | 237.5 | 246.5 | 236 | 349 | 530 |

| *XAG/USD(Silver) | 54.7 | 43.9 | 43.3 | 34.7 | 28.2 | 29.1 | 62.9 | 62.6 | 63.1 | 58 | 89.5 | 120 |

*Note that the pip value of every standard lot of Silver, based on brokers with the contract size of 5000 oz, is $50. If we compare that with for example EUR/USD, which the pip value of 1 lot is $10, every pip of silver can affect your account 5 times more than EUR/USD.

The following video is an excerpt of this article. I tried to explain some concepts visually to make them more tangible.

Methodology Of The Study

In this study, I used ATR (Average True Range), one of my favorite indicators. Some use ADR to calculate average daily range which is the difference between the high and low of a series of candles or bars. That can be an option but it doesn’t include gaps.

Gaps are important because they are a part of the price movement. You can’t see them in higher timeframes or candles when they happen in the lower ones but they are still there.

Let’s say I want to calculate the average daily range for one year which is something between 260 to 263 candles. There are gaps between this range of candles that are part of the movement of that currency pair so you shouldn’t eliminate or ignore them. They are like invisible candles that do affect the market and make higher timeframes’ candles or bars along with the visible ones.

ATR is the smart one that can do the trick here. It includes gaps when it calculates the range of candles. If there isn’t a gap, it behaves like ADR and uses the difference between high and low as its calculation.

On the other side, if there is a gap, it includes that by choosing from these options:

- high-low

- high-previous close

- low-previous close

Whichever gives the larger amount, it picks that one so if there is a gap it’s calculated.

Why Is Average Daily Range Important?

The average daily range for currency pairs came to my mind a few months after I started forex way back. The reason that I wanted to know that was I didn’t know how to set the size of TPs and SLs for different currency pairs because I didn’t know the personality or volatility of most of them.

I knew a handful of them such as EUR/USD or GBP/USD and I’d just been familiar with the crazy GBP/JPY. Actually, the reason I started to think about this issue was when I stumbled upon the crazy one. I couldn’t understand why I got beaten by that over and over the first day I tried it, so I decided to learn about the volatility and personality of major and minor currency pairs.

The importance of volatility varies according to trading style. It’s not that important when you take long-term positions or you are a position trader or swing trader. On the other hand, it does matter most when you are a scalper or day trader.

Imagine you are a scalper and you have set a 5-pip SL for your strategy. You’ve also backtested that in eur/use and come to the conclusion that the strategy is a winning one with that setup. Would you gain the same result if you tested on gbp/jpy. I bet your win rate dropped dramatically because you may have more TPs, but there is the spread factor that decreases your winning positions.

On the other hand, if you are a long-term trader and you have larger limitations, a few extra pips won’t be such significant. Of course, knowing the volatility here can help you to take a better approach in choosing suitable SLs and TPs according to the different currency pairs and their personality and move range.

There is another side where the average daily range can be considered important particularly if you are a day trader or scalper. As you know, each currency pair move in a specific average range daily, so when your setup appears in the chart and if the currency pair hasn’t exceeded its ADR, the probability that you get result fast is higher.

Imagine we’ve found a setup in a currency pair with an ADR of 100. The currency pair has moved 20 pips so far and it has 80 to go on average. It has enough potential to move and make the result of our trade clear instantly or at least soon.

Again it may not important for swing or position traders but it defiantly important for a scalper who tries to find positions with quick results especially if you consider liquidity too.

I’ve written a post about the best currency pairs to trade in which I talk about liquidity and mixing that with volatility. you can find it here.

Without further ado, let’s take a look at the study I did for 28 major and minor currency pairs from 2014 to 2019 and answer some questions and then we’re going to dig deeper.

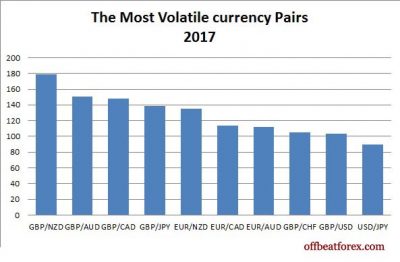

Which Currency Pair Is The Most Volatile?

The most volatile currency pair in Forex is GBP/NZD. It’s been the most volatile one since 2014 (the first year of this study)

GBP/NZD has shown a steady approach during these 6 years and has always been number one for this title. The maximum average daily range for this currency pair is 279 which is related to 2015, and the minimum ADR for it is 167, excluding 2019, which is related to 2018.

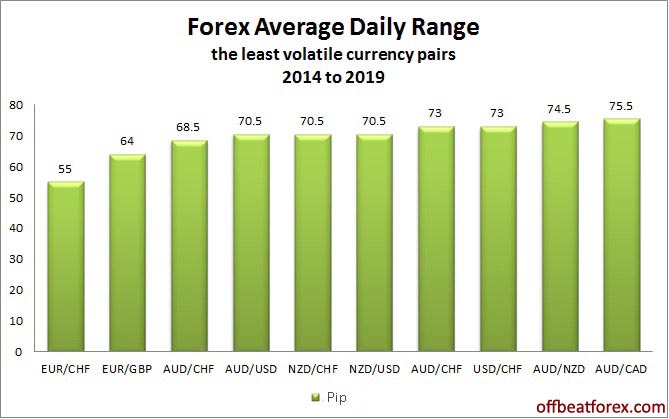

Which Currency Pair Is The Least Volatile?

The least volatile currency pair is EUR/CHF, however, in 2015 and 2018 it was the second least volatile one and changed its rank with EUR/GBP but the total daily average range, from 2014 to 2019, for EUR/CHF is less than EUR/GBP, therefore, it’s number 28 from 28 currency pairs and has the least volatility in total.

The maximum daily average range for EUR/CHF gets back to 2015 with 96 pips that brought it the rank of 25 and the minimum ADR for this currency pair is related to 2014 with as few as 23 pips, which is very low even for this pair.

What Are The Most Volatile Currency Pairs?

We talked about number one in our ranking but now let’s take a look at others. The most volatile currency pairs are (TOP 10)

- GBP/NZD

- GBP/AUD

- GBP/CAD

- GBP/JPY

- GBP/CHF

- GBP/USD

- EUR/NZD

- EUR/AUD

- EUR/CAD

- EUR/JPY

There are some replacements in ranking during this period but these currency pairs have always been in the top 10

- GBP/NZD

- GBP/AUD

- GBP/CAD

- GBP/JPY

- GBP/CHF

- EUR/NZD

- EUR/AUD

- EUR/CAD

GBP/USD, CHF/JPY, EUR/JPY, and USD/JPY are four other currency pairs that have competed with each other for two remaining spots in the top 10.

(Zoom in to see better)

In 2015 GBP/USD is replaced by CHF/JPY and in 2017 EUR/JPY is replaced by USD/JPY. Technically, GBP/USD and EUR/JPY are in the top 10 because they’ve been in this category 5 times out of 6 and the other two have been one out of six.

What Are The Least Volatile Currency Pairs?

The top 10 in the least volatile pairs are

- EUR/CHF

- EUR/GBP

- CAD/CHF

- AUD/USD

- NZD/CHF

- NZD/USD

- AUD/CHF

- USD/CHF

- AUD/NZD

- AUD/CAD

What Is The Maximum Of Forex Average Daily Range?

I also studied these Forex pairs from a different angle. It can help traders to make better decisions based on the maximum average daily range of currency pairs. It’s the maximum ADR from 2014 to 2018. I didn’t include 2019 because it doesn’t make any difference and actually, it’s from 2014 to 2019 August

How can max ADR help?

When a currency pair gets momentum based on some factors such as news, it starts moving faster and passing through its ADR and the next stop can be the max ADR.

It’s very unlikely that it goes beyond that level except there is one of the most volatile news such as NFP.

In normal conditions, if the price gets to that level, you should be more careful if you’ve found a setup because the price has run out of energy and it’s moved far more than its daily average, however, it can be a good opportunity to take advantage of corrections if your strategy allows and if you find a setup based on that.

What Are The Minimum Of Forex Average Daily Range?

On the opposite side, we have the minimum of the average daily range. It’s the minimum ADR from 2014 to 2019. It shows the least pips that the price of each currency pair can reach.

When a pair doesn’t have momentum and it’s ranging, min ADR is the first target after the release of energy and getting momentum. If a pair hasn’t made it to its min ADR yet, it’s the best time to take a position on it. The next stop after that would be ADR and then max ADR.

The best time of the day for this situation is before the overlapping of the sessions for each currency pair.

For example two hours before Tokyo session starts, Sydney session starts, so after two hours of opening of Sydney trading market, it overlaps with Tokyo and if we can find a setup in AUD/JPY before opening Tokyo, we can expect a range between min ADR, ADR, and max ADR depending on which level the pair has reached by then.

The Bottom Line

The difference between the average daily range of currency pairs shows their various potential movements, so it’s important to consider that when we want to set limitations (TPs and SLs) for our positions.

Therefore, if your strategy is profitable when you set 10 pips for your TP or SL in AUD/CAD and it isn’t profitable when you include EUR/NZD in your portfolio with the same limitations, you should reevaluate your limitations based on the new currency pair’s ADR.

Determining a static limitation for all forex pairs can be deadly to our win rate and it can turn a profitable strategy into a losing one.

Forex ADR can also be used as a gauge to show us the potential movement of every pair so it can help us to choose the best pairs to trade during a day. Generally, if a pair hasn’t passed its ADR level, there could be more opportunities to take advantage from.

It could be even better if it hasn’t crossed its min ADR. If the pair has gone beyond those levels and you still see potential according to a steep move generated from important news or any other factors, then you can consider the MAX ADR as your target.

let’s wind this post up with these questions:

The most volatile major currency pair in forex is GBP/USD with an average ADR of 111.5 pips from 2014 to 2025

The most volatile minor currency pair in forex is GBP/NZD with an average ADR of 201 pips from 2014 to 2025

The least volatile major currency pair in forex is shared between AUD/USD and NZD/USD, each with an average ADR of 70.5 pips from 2014 to 2019

The least volatile minor currency pair in forex is EUR/CHF with an average ADR of 55 pips from 2014 to 2019

Well done on all your great work here. You are doing great things and I think you

do you have adr table for crypto ?

No But not a bad idea, maybe in the future.

Hi David, really like your work. It helps my strategy and bot a lot. I have a question though: Is there a statistic you have where we will know how much the pair in max. pips travelled a day? Because Maximum Of Forex Average Daily Range does not really tell that, since it only tells the average. For me it is important how many times we went higher than average and how much % above average and/or maybe the average of all days and their pip counts when we are above average ADR in pips + the absolute max. pip count travelled in a day for that year.

I just checked on GJ for example and saw a strong rallye 6th December 2023 to 7th December. 360 Pips in total and there are days in the past years that even go far beyond that number (for example: Brexit)

Hi Aleksander,

There are a few ways you can do that. If you know how to code, you can use atr or adr formula, which is in the article above, to calculate the size of each candle and for example draw an arrow on the largest one in the last n days.You will probably find a script that does that if you search on mql or pinecoders communities.

There is also a simpler visual approach. use the atr or adr indicator with the period of 1. It basically shows the size of each candle (high – low). Then drag a horizontal line on the indicator and use the atr number in our table for the line. for example 164 (which is 1.64 in tradingview) for gj. Now you can see the largest daily candle’s size as well as the candles that are above and below adr, which is 164 in this case.Look at the atr and the yellow line in the pic.

Hi David

I just chanced upon your article and I must say that I’m really impressed with your work, and also for the fact that you take time to respond to your readers with detailed reasoning.

What is the ATR for DE40 for 2022?

Oh, and have you published your study for indices? I read in one of your responses that you intended to “…release it in a few days.” Kindly assist with the link if that you have completed it. Thank you.

Thanks for the kind words SEPATS. regarding your question, there are some reasons that I didn’t published the same study for indices but the main reason is I haven’t traded them, except for us30 of course. Since I’m not familiar with them then generally speaking I’m not qualified to write such a study. I’ve traded forex pairs and gold for many many years and I know them very well so I can write about them. There are many indices that I don’t know and moreover different brokers have different digit systems and even tickers for indices so making a general table might neither be comprehensive nor correct.

With that said, you can use the information in this article and use ATR indicator to find the average daily range for whatever ticker you want. Just open a daily chart, drop ATR on it, count the candles in one year (normally it’s between 259 and 263), set the counted number for ATR period (for example 260), and see the number that ATR shows. That’s the average daily range for your index. Feel free to ask any question if you need help with that.

Hi David,

Great job here.

What would you consider the most choppy pairs? Those that may be most suited for range trading.

Thanks,

Hey Anonymous…I’ve written an article about that. You can find it here

Hi David, I’ve been reading your material for some time now and just expressing my gratitude for the fantastic work you’re doing. Quick question, I thought your FX ADR Table data for 2022 was fixed once the new year started but I noted that it’s changed a few times even though we’re in 2023? Please kindly clarify. Also, will you be creating a 2023 column and charting the pairs throughout the year, or will you only do that at the end of 2023? Many thanks

Thanks, Ray. I update the table in the January of every year and only once. The next update will be in January 2024 when I’ll add the adr of 2023. The reason is a year must end so that we can have the entire data, around 260 to 261 candles/days. Changing that you probably refer to is the mistake I made this year. I was writing and testing indicators/strategies using MAs on the Pine script (tradingview platform). Right after that, I started finding adr for the table but I used the MA instead of ATR, mixed things up. The next day, I wanted to check the adr of some pairs that I noticed the mistake and fixed it.

Hi David.. Can we please know how to calculate, please? We need recent 12 months ATR and would to calculate at the end of every month. Is it based on any of your custom indicators? If yes, can we access them on tradingview

Hey Vuppala, add ATR to you chart on a daily timeframe. normally there are 259 to 261 daily candles in a year or 12 months, you can use “date range” tool on the tradingview to find out the number of candles as well, so the length of ATR is between 259 to 261. you don’t need to calculate anything, ATR does and on every new daily candle it’s updated.

Thanks David😆 This has taken my trading to the next level

Your welcome, happy to hear that.

HI David ! great job on your site !

…if i may make a suggestion…….if you desire so …can you add the 3 main American indices……+ the 3 main cryptos + the 2 main oil pairs ? ……..just a suggestion of course……but indices especially are being traded more and more…it would be nice to have all of these in your table ….i use an ADR on a separate chart to see this …but your table is so much more easier to read…….

Hey EP, yeah I’ll do that in few days

What is the average pip movement per day for us30 and nas100

The average daily range of US30 in 2022 is 549 and its 310 for nas100.

David I appreciate your good work. Please could I know the average pip movement of coffee and cocoa.

I’m doing similar analysis, and I needed this information! Thanks.

You’re welcome!

Hello, Thank you for your hard work! just wondering if you could add Nasdax 100 index

Excellent work David. Very impressed with your sharing. Keep up the spirit.

It is an eye opener for beginners like us. Amazing Job David Thumps up!!!!!

Happy to hear you found it useful

Hi David,

I just wondering if you would update the latest year of 2021, and also 2022. I just what to know if the EURJPY is trending upwards as far as the daily range (volatility is concerned) and to clarify daily range is the avg of all the major days (volatility ) which is open – close of the day? and also in your view does the volatility repeat in time over years? For EURJPY.

Thanks,

San

Hi San,

Yes, I will update the table at the end of 2021 and also for the next years.

The formula of the average daily range used here is mentioned in the methodology section. It’s the ATR formula which is high- low in case there is no gap. If there is a gap, that’s as mentioned in that section.

In the same economic condition, the volatility for a pair can be repeated to some extent but if an unusual economic situation such as recession happens, it changes the volume traded and consequently volatility.

You have done a wonderful job. Appreciate so much for your hard work and effort.

You have made many people interested and happy.

Best wishes to you.

Thanks Yen, happy to hear

Hi David,

Greatly appreciate your layout of the Daily Ranges. It has helped me quite a bit. Any idea where I can get my hands on Weekly Ranges? Thank you in advance.

Hi Jarred,

Glad to hear it helped you. You can use an ATR with the period of 50 or 52 (number of weeks in a year) on weekly charts. It gives you the average weekly range for any pair you want.

Very great job

Thanks

Hi David,

I am very impressed with your work. Great Job on ATR. I have a question for you. What value do you use in ATR lengths? How many days of data to figure out the ATR. I hope I am making sense here. I tried for 30 days. I am still not getting the numbers that you have listed for an average daily range.

Hi David

I appreciate you answering my question. I tried 260 and 261 I get the ATR 117 and 118 for GBPUSD. You have at 141. How do I get that number 140 or 141?

What number should I input in my ATR?

I still don’t know what number I should input in my ATR to get 131 or 141 FOR GBPUSD. You have 141 on your site. What do you input on your ATR to reach that number. ATR 260? Or 30. I cannot figure it out. Appreciate your help and answer

I see that you have updated the data for ATR. Thanks

Hi David,

I have linked this study in a response to a trader question on Baby Pips forum. It actually answers one of many questions I had as I build my detailed trading plan after a four year absence from trading. Thank you for your valuable study.

Glad to hear that

Hello. If Daily ATR or 1H ATR is 30 pips let’s say…our SL and TP should be 30 pips when we enter a trade or something like 15 pips?

Thanks.

It’s a general question. Setting tp and sl depend on your strategy, winrate, RR; however, as a general rule, the amount of ATR for SL is equal to 1x of atr (where x is the amount of atr). for example, if your trading timeframe is 1h and the atr shows 30 pips, your sl should be 30 pips. regarding tp, it depends on the RR (risk/reward) of your strategy, it can be 1x,1.5x,2x, and etc. One of my strategies has 1.5x and another one has 2x. using atr for sl, in general, means your sls’ tolerance level is x average range. for instance, you draw a trendline and put your sl, which is 1x atr, under that. the price might penetrate in the line but pull back and act as a shadow. it’s assumed it doesn’t go further one average candle and the shadow isn’t longer than an average candle.

Hi.

Interesting stuff you got here brother. I was just watching trading in the zone. And so much is related to your study. Thank you.

Regards Dhiren

Do you have YouTube video that explain it sir?

Then What is the best pair for scalping ?

I don’t understand!

I also have a question!

What is the difference between the chart entitled “Forex Average Daily Range” and the chart entitled “The Most Volatile Currency Pairs”? For example: The chart entitled “Forex Average Daily Range” shows GBPNZD as 201 Pips and in the chart entitled “The Most Volatile Currency Pairs” shows GBPNZD as 1200. If 201 is the daily average what is 1200, is it the monthly aveage or yearly average or what? I don’t understand the difference. It is not explained in the text.

That’s the total pips or movement of the pairs from 2014 to 2019. It was related to the process of calculation before averaging the 7 years. I was working on a 7-candle circle, instead of 5, for a week and the pictures were for that — nothing important.

Nice! I been thinking of doing a similar study as I want to know the most volatile currency pair to trade but you have done such a great job and more complete than I probably would have thought to do. Much appreciated keep up the good work!

Thanks, I’m glad that it can help you

Such a beautiful Job.. Thanks so much for the insight.

hi, can u also share the volatile for XAU/USD @ gold ?